PSAT/NMSQT Prep 2022 - Eggert M.D., Strelka A. 2022

How much do you know?

PSAT reading passage strategies

PSAT Reading

LEARNING OBJECTIVES

After completing this chapter, you will be able to:

· Identify keywords that promote active reading and relate passage text to the questions

· Create short, accurate margin notes that help you research the text efficiently

· Summarize the big picture of the passage

How much do you know?

Directions: In this chapter, you’ll learn how PSAT experts actively read the passage, take notes, and summarize the main idea to prepare themselves to answer all of the passage’s questions quickly and confidently. You saw this kind of reading modeled in the previous chapter. To get ready for the current chapter, take five minutes to actively read the following passage by 1) noting the keywords that indicate the author’s point of view and the passage’s structure, 2) jotting down a quick description next to each paragraph, and 3) summarizing the big picture (the passage’s main idea and the author’s purpose for writing it). When you’re done, compare your work to the sample passage map that follows.

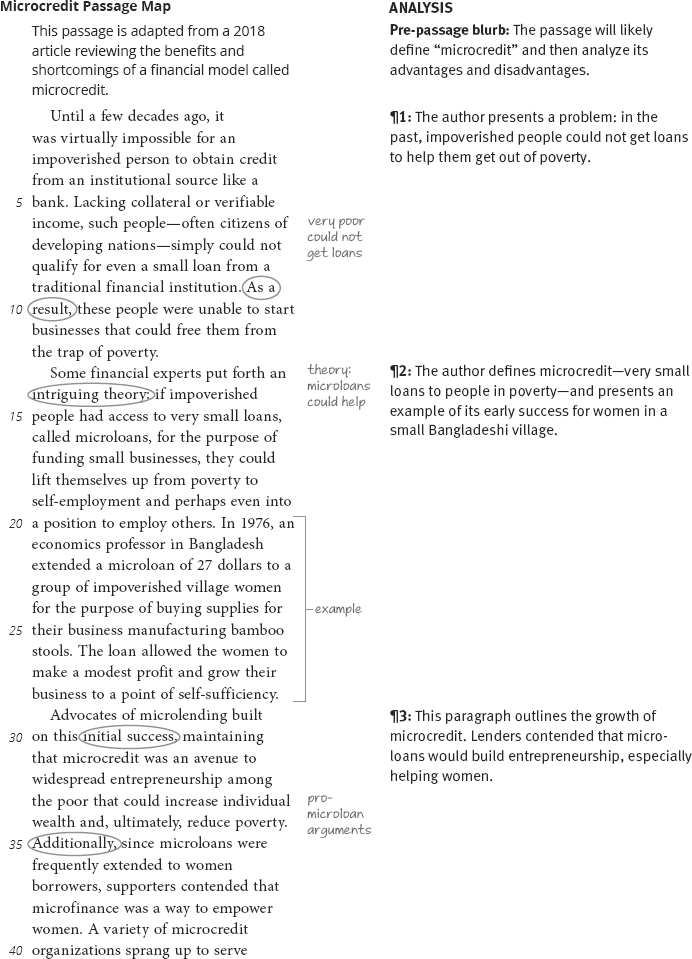

This passage is adapted from a 2018 article reviewing the benefits and shortcomings of a financial model called microcredit.

1Until a few decades ago, it 2was virtually impossible for an 3impoverished person to obtain credit 4from an institutional source like a 5bank. Lacking collateral or verifiable 6income, such people—often citizens of 7developing nations—simply could not 8qualify for even a small loan from a 9traditional financial institution. As a 10result, these people were unable to start 11businesses that could free them from 12the trap of poverty.

13Some financial experts put forth an 14intriguing theory: if impoverished 15people had access to very small loans, 16called microloans, for the purpose of 17funding small businesses, they could 18lift themselves up from poverty to 19self-employment and perhaps even into 20a position to employ others. In 1976, an 21economics professor in Bangladesh 22extended a microloan of 27 dollars to a 23group of impoverished village women 24for the purpose of buying supplies for 25their business manufacturing bamboo 26stools. The loan allowed the women to 27make a modest profit and grow their 28business to a point of self-sufficiency.

29Advocates of microlending built 30on this initial success, maintaining 31that microcredit was an avenue to 32widespread entrepreneurship among 33the poor that could increase individual 34wealth and, ultimately, reduce poverty. 35Additionally, since microloans were 36frequently extended to women 37borrowers, supporters contended that 38microfinance was a way to empower 39women. A variety of microcredit 40organizations sprang up to serve 41the needs of the poor in Asia, Latin 42America, Africa, and Eastern Europe.

43A number of different microlending 44business models developed, and over 45the ensuing decades, the number of 46customers of microcredit grew from 47a few hundred to tens of millions 48worldwide. Microlenders and 49microcredit advocates told stories of 50desperately poor people who had lifted 51themselves out of poverty and into 52self-sufficiency, and of impoverished 53women who had become family 54breadwinners through the use of 55microloans. Microfinance, it seemed, 56was a tremendous success.

57Soon, however, another side of 58the story came to light. Anecdotes 59emerged about impoverished borrowers 60who were unable to pay their interest 61from their business earnings, became 62imprisoned in debt, and were forced to 63sell off their meager possessions to meet 64their loan obligations. Other stories 65described customers who used their 66loans for consumption spending rather 67than to finance businesses, and who 68were thus unable either to pay their 69interest or to return the original money 70borrowed. A backlash developed against 71microlending. Members of the media, 72politicians, and public administrators 73harshly criticized the industry and 74its advocates for promoting a process 75that could harm rather than help the 76neediest and most vulnerable people.

77Nevertheless, economists were 78more cautious. They recognized that 79anecdotes were not adequate to support 80either side of the debate meaningfully. 81What was needed was solid scientific 82evidence that could quantify the 83real impacts of microlending. 84Academics focused on finance and 85development performed a number of 86studies exploring various aspects of 87microfinance.

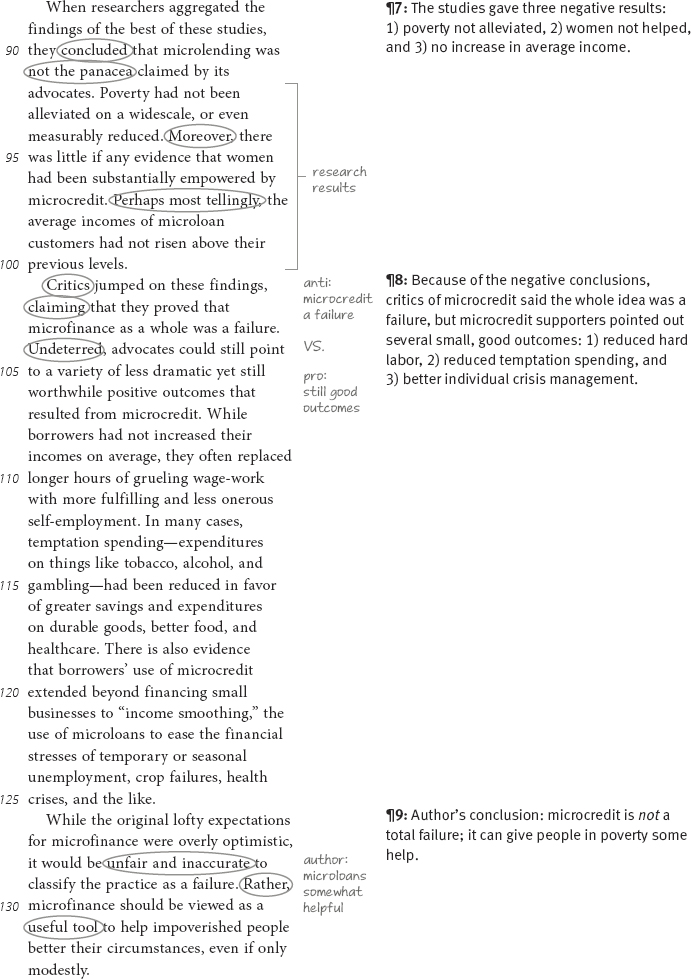

88When researchers aggregated the 89findings of the best of these studies, 90they concluded that microlending was 91not the panacea claimed by its 92advocates. Poverty had not been 93alleviated on a widescale, or even 94measurably reduced. Moreover, there 95was little if any evidence that women 96had been substantially empowered by 97microcredit. Perhaps most tellingly, the 98average incomes of microloan 99customers had not risen above their 100previous levels.

101Critics jumped on these findings, 102claiming that they proved that 103microfinance as a whole was a failure. 104Undeterred, advocates could still point 105to a variety of less dramatic yet still 106worthwhile positive outcomes that 107resulted from microcredit. While 108borrowers had not increased their 109incomes on average, they often replaced 110longer hours of grueling wage-work 111with more fulfilling and less onerous 112self-employment. In many cases, 113temptation spending—expenditures 114on things like tobacco, alcohol, and 115gambling—had been reduced in favor 116of greater savings and expenditures 117on durable goods, better food, and 118healthcare. There is also evidence 119that borrowers’ use of microcredit 120extended beyond financing small 121businesses to “income smoothing,” the 122use of microloans to ease the financial 123stresses of temporary or seasonal 124unemployment, crop failures, health 125crises, and the like.

126While the original lofty expectations 127for microfinance were overly optimistic, 128it would be unfair and inaccurate to 129classify the practice as a failure. Rather, 130microfinance should be viewed as a 131useful tool to help impoverished people 132better their circumstances, even if only 133modestly.

BIG PICTURE

Main Idea: Microcredit provides some relief for impoverished people even if it is not the total success its supporters imagined.

Author’s Purpose: To analyze the claims of microcredit advocates and critics in light of research on the subject